Millennials, born between 1981 and 19961, are coming of age. With age, comes a laundry list of questions: How am I going to pay down my student loans? What is a retirement fund? Should I continue to rent or is it the right time to buy a home? Is it a boy or a girl?

Millennials, born between 1981 and 19961, are coming of age. With age, comes a laundry list of questions: How am I going to pay down my student loans? What is a retirement fund? Should I continue to rent or is it the right time to buy a home? Is it a boy or a girl?

The many unknowns during this period in life can feel exciting and a bit daunting at the same time. We don’t have all the answers, but we have learned over the years that proper financial planning and guidance can help young investors prepare for life’s curveballs and enjoy the ride along the way. In this article, you will find tips, tricks, and best practices that may help make this period in life a bit easier and help you plan for long-term financial success.

ESTABLISH A RESERVE FUND

As soon as you land your first “adult” job, it’s time to begin saving. Determining a monthly budget is the first step, and this starts by understanding how much is needed each month for heat, electric, cable, internet, food, transportation, vehicle maintenance, and any debt obligations. Once a budget is known, then aim to save at least 6 months worth of these expenses in an accessible and liquid account such as a savings account at a bank or credit union. While it may not feel like the most exciting use of your newfound earning potential, a reserve fund can come in handy when life’s surprises show up.

TAKE ADVANTAGE OF EVERY EMPLOYEE BENEFIT

Many employers today provide health and dental insurance, a retirement savings plan, and vacation time, as well as other benefits and perks. While retirement and healthcare may seem like concerns to address in the distant future, it’s critically important to set yourself up with good healthcare coverage as soon as possible and begin taking advantage of your company’s retirement savings plan.

In many cases, employers will “match” a certain percentage of the monthly contribution you make to your retirement savings account. For example, if you decide to contribute earnings into your company’s 401(k) plan, your company may match your contributions dollar-for-dollar up to a designated percent (e.g., 4%). Many young investors pass on saving for retirement, simply because they would rather have this money in their pockets today instead of in retirement savings accounts for the next three decades.

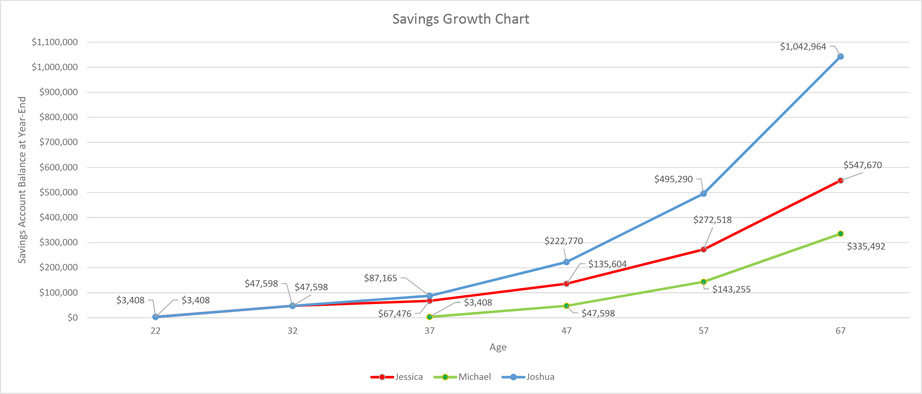

Research and our personal experience have shown time and time again that the earlier you can start saving for retirement, the better. Just consider the following which shows the financial growth of three individuals, each of whom has chosen a different approach to saving. Under each of these scenarios, contributions are assumed to be made at the end of the month, and earnings are compounded monthly at the end of the month using an annual rate of 7%.

- Jessica contributes $275 monthly between the ages of 22 and 32. During that 10-year period, she builds a retirement balance of $47,598. Over the next 35 years, the compounded interest tied to the annual rate of 7% grows her balance to approximately $547,670.

- Michael decides to start saving at age 37 (15 years later than Jessica) and contributes $275 monthly between the ages of 37 and 67. His balance grows to approximately $335,492. This illustration demonstrates the importance of saving as early as you can as Michael does not build a retirement balance as high as Jessica’s, who only saved for 10 years but at a much earlier age.

- Joshua decides to steadily contribute $275 monthly over 45 years from age 22 to age 67. By starting early and making steady contributions over the course of 45 years, he builds a retirement balance of approximately $1,042,964 by the time he reaches age 67.

The above scenarios and chart are hypothetical, and are not intended to represent any particular savings or investment vehicle. They do not take into account any taxes, fees, or any other costs or deductions.

DON’T RAID YOUR GROWING NEST EGG

While your retirement accounts grow, it can be tempting to spend these savings. It’s important to understand that, under usual circumstances, withdrawals taken from these accounts before age 59 ½ will be taxed as ordinary income and subject to an additional 10% penalty. For example, if you take an early withdrawal of $10,000 from your retirement account and are in the 20% tax bracket, you would be required to pay $2,000 in taxes (20%) plus $1,000 as a result of the 10% penalty.

What started out as a $10,000 “payday” now amounts to $7,000 in your pocket and a retirement savings account which is $10,000 lighter.

Understandably, these withdrawals can have significant long-term impacts on your ability to comfortably retire some day. For this reason, we generally recommend that young investors avoid early withdrawals when at all possible. If you are considering taking an early withdrawal, consult a trusted financial advisor to see what alternative options may exist.

DEVELOP A SOLID PLAN TO PAY DOWN DEBT OBLIGATIONS

One of the biggest challenges young millennials face is repayment of their student loans. Upon joining the workforce, there is a high likelihood that you will still be carrying student debt. Unlike your retirement savings account, compound interest is now working against you. It’s important to understand the types of loans you have outstanding, as this will impact which paydown strategy will be most effective. For example, there is a 6-month grace period with federal subsidized loans, whereas the interest clock starts ticking immediately for private loans.

Attack your student loans with a plan, and start by setting a realistic paydown deadline for yourself. Making an extra payment or two each year will reduce the lifetime cost of these loans. You will likely accumulate more debt throughout your life, so use this process as a learning experience. Again, a trusted advisor can help make this process a good learning experience that can be applied elsewhere in your life.

TIPS WHEN BUYING YOUR FIRST HOME

Buying a home is not a spontaneous decision, and a savvy home purchase may provide a return on investment later in life. Be prepared and avoid living outside of your means when choosing your first home. It’s always wise to watch the housing market, be aware of lending rates, and start saving while you remain “on the sidelines.”

A home may be the first big investment you make in your adult life

When it comes to making a down payment, keep in mind that your monthly mortgage rate will be higher if you can’t put 20% down. You may also be subject to paying private mortgage insurance (PMI). If you can’t put 20% down, research your potential lenders and any promotions that they may offer. Some banks and credit unions offer special programs to first-time home buyers that can reduce or even eliminate the PMI expense.

STARTING A FAMILY IS EXPENSIVE, BUT WORTH THE COST

Many times, buying a home and starting a family go hand-in-hand. They are turning points that represent huge strides into adulthood. When you get married, you are now responsible for the well-being of another person in addition to yourself.

At this stage in your life, insurance becomes much more important. You and your spouse should sit down with a planner to review each other’s health insurance policies and determine how much coverage your family will need moving forward. If one policy offers a significantly more attractive plan than the other, the two of you may benefit from a switch to family coverage. When your children are born, one or both of you will need to provide family coverage.

Purchasing a life insurance policy may also make sense. Should you or your spouse unexpectedly pass away or become disabled, adequate coverage will help to cover the financial burden on your family moving forward.

With growing college tuition costs, saving for your children’s higher education is more critical than ever before. When you have children, start saving for their college tuition at the time of birth. There are many college savings strategies to choose from, like 529s, ESAs, and UTMAs. Each comes with different benefits and limitations. Again, it’s always a wise decision to consult a trusted financial advisor who can help shape the best course of action.

DO NOT FORGET ABOUT WORK/LIFE BALANCE

Who said life should be all work and no play? We should be able to enjoy ourselves now, too!

That does not mean burning through your paycheck in a weekend. Leisure time can be enjoyed responsibly by building enjoyable activities into your budget. Dedicating a small percentage of your paycheck each period specifically for travel, leisure, and entertainment will allow you to maintain your mental health without significantly impacting your finances.

ASK FOR HELP WHEN YOU NEED IT

Each generation has different questions that need answering. As we age, those questions change. In our 20s and 30s, we are still finding ourselves and looking for our niche. Life tends to throw us into situations we could have never seen coming, but setting goals and planning for the unexpected will help you better handle these questions.

Take time to build a budget for your expenses, emergency fund, retirement, home, college costs, leisure, and any other important financial aspect of your life. Start saving young, add regularly, and allow compounding interest to be your friend. Lastly, always consult a professional when you need guidance. If you take the time to follow this advice, your future-self and family will thank you.

1Pew Research Center, Defining generations: Where Millennials end and post-Millennials begin

You may also like